A reverse home mortgage is a home loan made by a home mortgage loan provider to a house owner using the house as safety or security. Which is considerably different than with a traditional mortgage, where the property owner uses their revenue to pay for the debt in time. Nevertheless, with a reverse home mortgage, the car loan amount expands over time because the home owner is not making regular monthly home mortgage settlements.

When you die, market your house, or leave, you, your spouse, or your estate would repay the loan. In some cases that suggests marketing the house to get cash to pay back the lending. As with a forward home loan, the home is the collateral for a reverse mortgage. When the homeowner relocates or passes away, the profits from the house's sale most likely to the lender to pay back the reverse home mortgage's principal, interest, mortgage insurance policy, and costs. Any sale continues past what was obtained go to the home owner or the home owner's estate.

Keep in mind that the adjustable-rate HECM provides every one of the above payment options, however the fixed-rate HECM only offers lump sum. In a 2010 survey of elderly Americans, 48% of participants mentioned financial troubles as the main reason for obtaining a reverse home mortgage and also 81% stated a wish to continue to be in their existing homes up until fatality. Continue reading to get more information concerning exactly how reverse home loans function, getting a reverse home loan, getting the best deal for you, and just how to report any type of fraud you could see. A home equity financing is a consumer lending secured by a second mortgage, permitting house owners to borrow against their equity in the residence. The average borrower's first major restriction has to do with 58% of the optimum insurance claim quantity. The lending profits are based upon the age of the youngest customer or, if the consumer is married, the more youthful spouse, even if the younger partner is not a borrower.

- Our objective is to offer viewers with accurate and honest details, and also we have content criteria in place to make sure that takes place.

- Typically, consumers or their beneficiaries repay the lending by offering your home securing the reverse home mortgage.

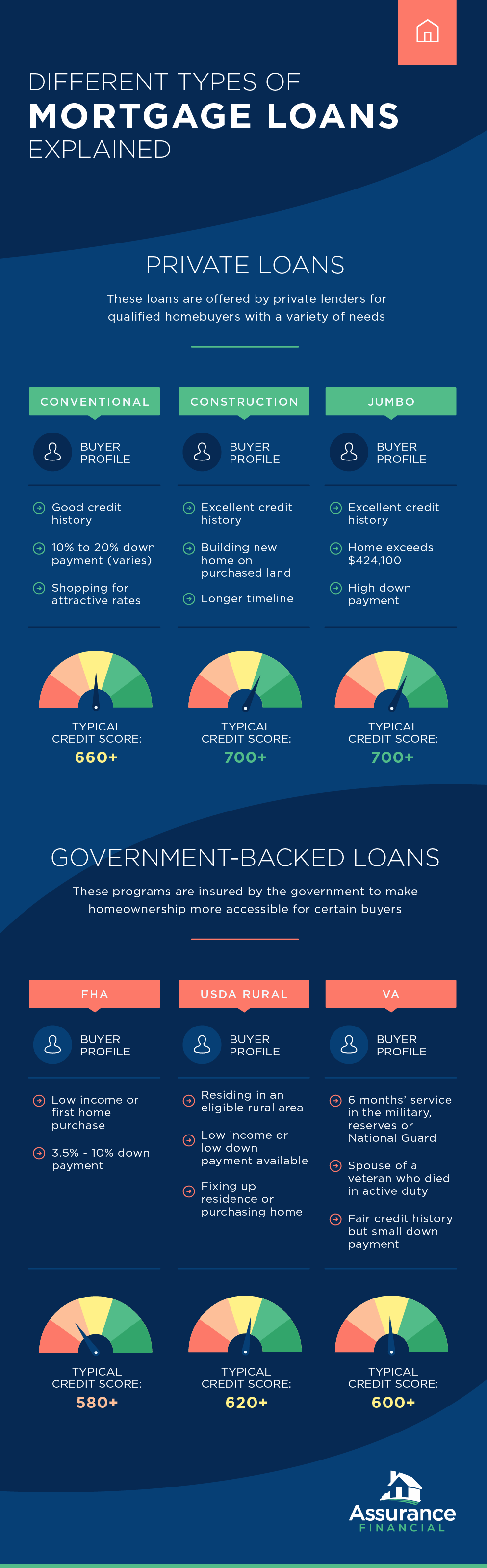

- As a matter of fact, if you're not yet 62, a residence equity financing or HELOC is likely a much better alternative.

- HUD does have minimum credit report demands for the reverse mortgage that takes the consumer's total desire as well as capacity to pay their debts as well as manage their home right into factor to consider.

- If you have strategies to move later on in retirement you should consider options such as the reverse mortgage for house purchase, or other residence equity finances.

- But this compensation does not affect the information we release, or the testimonials that you see on this site.

You need to comprehend how it functions as well as exactly how it could suit your funds to make a decision whether it's right for you. In addition to that, since the IRS thinks about a reverse home loan a funding, not real earnings, it additionally won't be counted in solutions that use your revenue, such as impacts to your Social Protection and also Medicare advantages. Prior to you decide, below's what you need to learn about reverse home loan benefits and drawbacks. A reverse home mortgage is a method to transform several of your home's equity right into cash. Visit the Attorney General's web site to find out more about reverse home loans and various other issues of rate of interest to seniors. The amount you can borrow is based on your home's value, present rates of interest, as well as your age.

Reverse Home Loan Lenders

If the spouse of the principal debtor is a co-borrower on the reverse home loan, they are allowed to stay in your house without paying back the funding. If you choose a federally backed option, you will certainly likewise be required to pay mortgage insurance coverage premiums. These costs can be secured of the loan amount, so you do not need to pay them out of pocket, however wesley mutual, llc they will minimize just how much cash you receive after closing.

How To Pay Back A Reverse Mortgage After Death

A cash-out re-finance replaces your current home mortgage with a brand-new financing that has a higher balance, which enables you to pocket the distinction in cash. Traditional as well as FHA cash-out refinances allow you to borrow approximately 80% of your home's value. Eligible army borrowers may qualify to tap approximately 90% of their residence's value with a cash-out re-finance assured by the united state . A house equity financing funding allows you to borrow as much equity as you need in a round figure with a fixed-rate settlement.

You can pick to receive your repayments as long as you stay in the home, or you can set up a set term to obtain payments. It's even feasible to utilize a credit line for your reverse home loan. Regardless of what kind of payment configuration you choose, you can't be compelled to market your home to settle the home mortgage, as well as you won't need to pay until you no more stay in the residence. On the other hand, though, doubters explain that reverse home mortgages often include high fees, as well as finance equilibriums boost gradually. In addition, reverse mortgages that aren't made through an FHA program may do not have some consumer securities, which might leave you responsible if the residence loses value.

If the reverse home mortgage comes due as a result of living beyond the residence, also unwillingly as a result of clinical Additional resources demands, you might not have the funds to pay off the reverse home mortgage as well as may shed your residence. In the event of your death, your successors will be responsible for settling the reverse home mortgage with various other funds from your estate, their very own funds, or earnings from the sale of the home. This deal is likely to be just in the supposed best interest of the financial Visit this website expert, loved one, or caregiver. These are simply a few of the reverse home loan frauds that can trip up unwitting home owners. It's an excellent idea to request a reverse home loan with a number of business to see which has the lowest prices as well as charges.

Rates can differ depending on the lender, your credit rating and also various other elements. The quantity you obtain will certainly likewise be influenced if the house has any kind of various other home mortgages or liens. If there's an equilibrium from ahome equity loanorhome equity line of credit, for example, or tax obligation liens or judgments, those will certainly need to be paid with the reverse home loan profits initially. You need to have the monetary capability to remain to pay on property taxes, home owners insurance as well as property owners association charges. Home owners who opt for this type of mortgage don't have a monthly payment and don't have to market their house, yet the finance needs to be paid off when the debtor dies, completely leaves or offers the home.