In the last few years, with rate of interest hovering at record lows, consumers that had a variable-rate mortgage reset or changed didn't see as well big a jump in their regular monthly settlements. But that can transform depending on how much and also exactly how rapidly the Federal Reserve increases its benchmark price. To get a grasp on what remains in store for you with a variable-rate mortgage, you first need to understand exactly how the item works.

- These complexities can present risks for consumers that do not fully recognize what they're entering into.

- " Most of my customers have been using ARMs," claimed Abby Ronquillo, owner of NetRealty in Corona.

- Realty representatives as well as mortgage brokers say the funding program is different this time around around.

- If that occurs, you may intend to take into consideration refinancing right into a fixed-rate or a brand-new adjustable rate mortgage.

- Lock Your Price With Rocket Mortgage ® by Quicken Loans ®, start your home loan application as soon as possible by responding to just a few basic questions regarding your objectives.

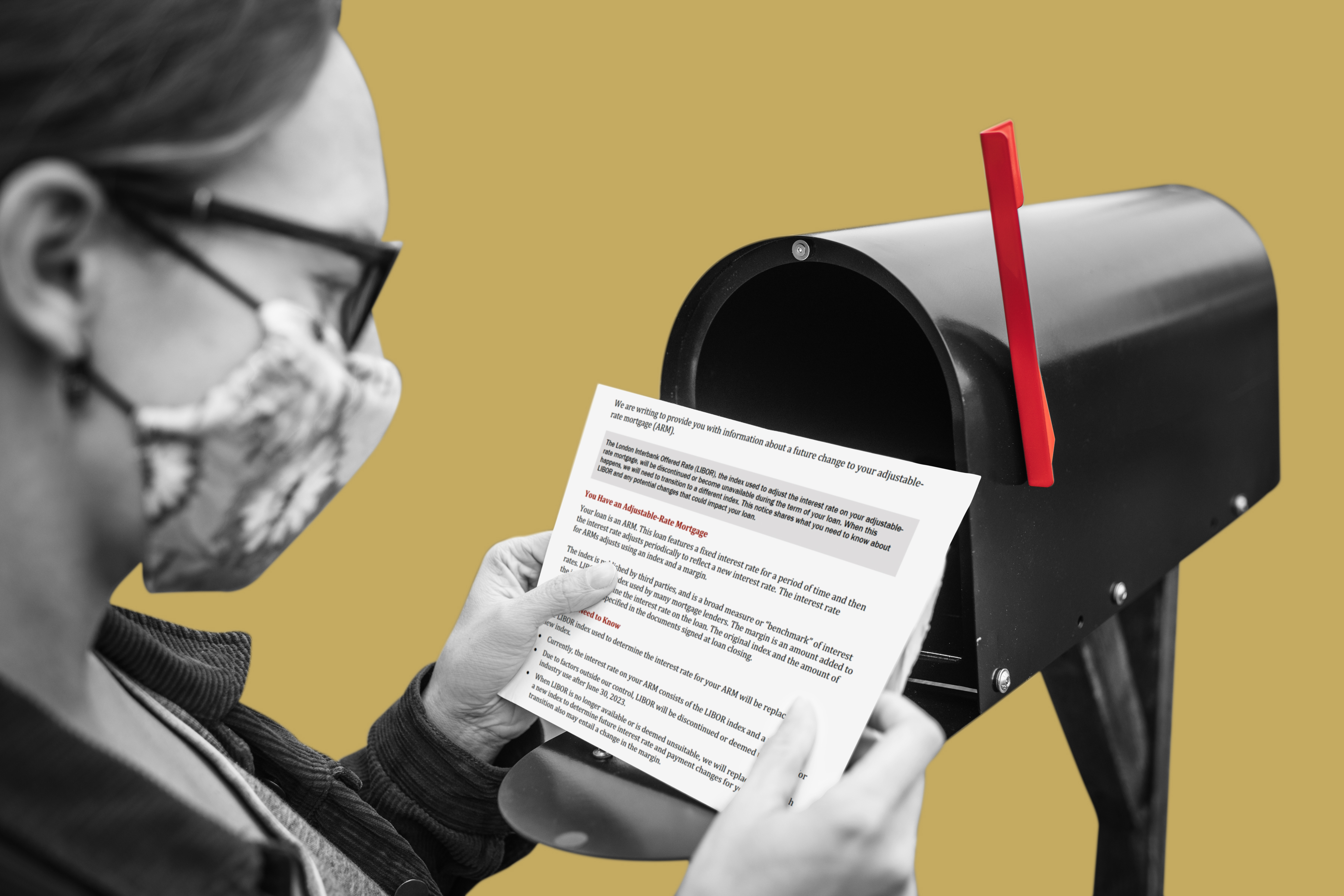

- Reset day is a moment when the preliminary fixed interest rate on a flexible price home loan changes to a flexible price.

Most ARMs use a 5% life time modification cap, but there are greater life time caps that might eventually cost you far more. If you're taking into consideration an ARM, ensure you totally comprehend just how price cap quotes are formatted and also exactly how high your regular monthly settlements could obtain if interest rates climb up. Alternative ARMs are often provided with a really reduced teaser price (often as low as 1%) which converts right into very low minimum payments for the first year of the ARM.

For lots of people buying a residence, rate and area are leading considerations. Just how much a financial institution is willing to provide-- as well as under what problems-- likewise plays a role in determining what they can manage. That's why it is necessary to assume timeshare attorney reviews purposefully, specifically with rates near historically low levels. NerdWallet strives to maintain its info exact and also approximately date.

Whats The Difference In Between Arms As Well As Standard Home Loans?

These caps operate relative to exactly how commonly their interest rate modifications, just how much it can rise from duration to duration, as well as an overall passion boost over the life time of the financing. Although it might seem like an intro price, your spending plan will certainly take pleasure in the preliminary low monthly repayments. With that, you might have the ability to put more towards your major every month. The margin put on your ARM depends on your credit rating and also credit report, as well as a basic margin that identifies home mortgages are naturally riskier than the types of financings indexed by the benchmarks. One of the most creditworthy consumers will certainly pay close to the conventional margin on mortgages, and also riskier car loans will be further marked up from there. A fixed-rate home mortgage can supply even more certainty due to the fact that it keeps the rachel ansley same rates of interest for the life of the loan.

Different Types Of Arm Financings

That didn't happen, as well as the memory of the result has continued to be clear. Interest-only ARMs and choice ARMs are various other methods property buyers can begin with low repayments however end up with a lot higher repayments down the road. You've reached focus on modifications in the fed funds rate and short-term Treasury expense returns, due to the fact that LIBOR normally transforms in lockstep with it. An adjustable-rate mortgage is a car loan that bases its interest rate on an index, which is normally the LIBOR rate, the fed funds rate, or the one-year Treasury bill. An ARM is also referred to as an "adjustable-rate car loan," "variable-rate home mortgage," or "variable-rate lending." Nevertheless, there are some kinds of fundings that she would recommend property buyers prevent.

It's worth noting that ARMs make up 18% of all home mortgages in California, a verification that in the most costly edges of an expensive market, people should be as critical as feasible. The couple had been outbid on the initial residence they shopped as well as really did not wish to run the risk of losing out once more. So when they place in an offer on the townhouse, they bumped it to $30,000 above the asking price, despite the fact that the settlements might strain their budget. That came to be troublesome, nevertheless, when the housing market crashed as well as the ARMs reset to higher rates that those buyers could not deal with. If your suggestion of huge risk is biting right into a truffle without asking what flavor it is, you most likely want a longer fixed duration. If you have actually got a five-year plan, for instance, a 7/1 ARM may assist you rest a little much better in the evening.

After that, your rates of interest might change every 6 months, depending upon the marketplace. That wesley mortgage implies your month-to-month mortgage payment can rise or down twice a year. Your rate won't increase more than 5% of the original rate throughout the life of the finance, though.

Secure Your Rate

This can cause challenge on the debtor's part if they can't manage to make the brand-new payment. ARMs have a fixed period of time throughout which the first rate of interest remains consistent, after which the rates of interest changes at a pre-arranged frequency. The fixed-rate period can differ significantly-- anywhere from one month to ten years; shorter modification periods generally bring reduced initial rates of interest. After the first term, the lending resets, suggesting there is a new interest rate based on present market prices.